I. Overview

| Name |

BOC Zhai Shi Tong Wealth Management Plan |

| Short Name |

BOC Zhai Shi Tong |

| Code |

830100 |

| Establishment Date |

May 26, 2010 |

| Type |

Non-principal guaranteed, with a variable yield |

| Investment and Returns Currency |

RMB |

| Manager |

Bank of China Limited |

| Custodian |

Bank of China Limited |

| Investment Objective |

This product mainly invests in high credit rating bonds with stable returns and high liquidity on domestic market. With Bank of China as its manager, the investment objective is to provide a bond product with high returns and liquidity and to develop a professional investment channel on domestic bond market by balancing risks and returns and relying on the expertise and investment ability of the bank. |

| Performance Benchmark |

After-tax interest rate of one-year time savings deposit |

| Duration |

None |

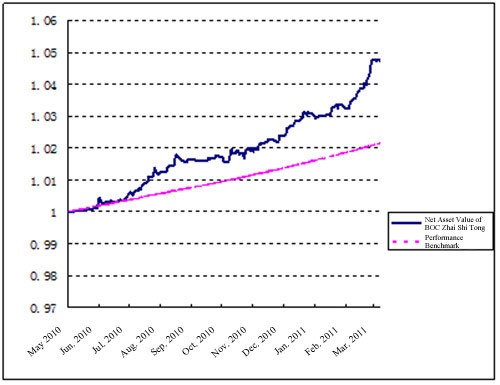

II. Net Asset Value (As of March 31, 2011)

The net asset value and yield of BOC Zhai Shi Tong from its establishment date are shown below (management fee and custodian fee deducted):

| Net asset value per share (March 31, 2011) |

1.0474 |

| Annualized yield from the establishment date |

5.60% |

| Accumulated yield from the establishment date |

4.74% |

| Performance benchmark x accumulated yield from the establishment date |

2.14% |

| Accumulated yield - performance benchmark |

+2.60% |

Note: The performance benchmark is the after-tax interest rate of one-year time savings deposit.

The following graph shows the net asset value per share of BOC Zhai Shi Tong and its performance benchmark from the establishment date (May 26, 2010 to March 31, 2011):

III. Bond Market Analysis and Investment Operation during the Reporting Period

During the reporting period, the transaction volume on domestic bond market fell first and then rose. The inflation expectation and deflation policy once suppressed the bond market, but bond purchase by institutions at low prices gave it a stimulus. As a result, the yield of bonds with different terms fell.

The short-term market rate has risen significantly since mid January, and the 7-day repo rate has held at 7% for nearly two weeks, with an unprecedented high of 8.5%. The monetary market rate fluctuated abnormally due to a large amount of money retreating from the banking system during the Spring Festival holiday and PBOC raising the reserve requirement ratio before the Spring Festival. During the Spring Festival holiday, with a relatively flat yield curve, the short-term bonds (less than one year) rose greatly, while the medium- and long-term bonds rose slightly. In late January, the 3-year central bank notes reached a yield up to 3.78%, and the 10-year T-bonds held a yield about 4%. On February 9, the yield of T-bonds with a term ranging from 3 to 10 years rose by 10 bps as a result of the inflation control operation by People's Bank of China (PBOC): a sudden interest rate rise after the holiday. However, with a background of money flowing back into the banking system, ample capital on the inter-bank bond market, and an uncertain international situation, the yield on the bond market fell to the level before interest rate rise. On February 21, the Political Bureau of the CPC Central Committee decided at a meeting that the country should maintain stable and consistent macro-economic policies while improving accuracy, flexibility and efficiency of the policies, as well as keep overall price levels basically stable. The market learned that "maintain stable and consistent macro-economic policies" was at least as important as "inflation control". On the other hand, the oil prices rose against the rising tensions in Middle East and North Africa. Furthermore, HSBC China's PMI fell to a 7-month low of 51.7, resulting in a market concern sentiment on the fundamentals. Consequently, the bond market experienced another round of rise: 10-year T-bonds broke below 4% barrier to around 3.90%; 3-year central bank notes fell below 3.70% from a high above 3.8%. In March, with an increasing capital on the inter-bank bond market, the yield of all bonds involved in bond transactions fell, while bond purchase by institutions warmed up. The interest rate on the primary and the secondary bond market decreased in turn. The yield of 2 to 3-year central bank notes fell to within the range of 3.55 to 3.60%; 3-year financial bonds to around 3.80%; 5-year financial bonds to 4.0%, 10-year T-bonds to around 3.90%. Meanwhile, with abundant capital on the market and a large volume of matured bonds on the open market, the 7-day repo rate bottomed to 2.05%, and the overnight repo rate fell to 1.70%, all of which recorded the historical low of 2011.

In respect of investment management, under a high pressure of microeconomic regulation and control and commodity prices, the bank, guided by balance of returns and risks, actively carried out operations depending on price waves on the basis of fully understanding the market sentiments and expectation deviation: seizing trading chances against the impact from rise of interest rate and reserve requirement ratio; increasing investment in short- and medium-term debenture bonds to improve the overall yield; earning a higher yield by purchasing debenture bonds on the primary market to lift the net asset value of the product greatly.

IV. Outlook of Bond Market and Investment Strategy

Although the bond market experienced a short-term bounce, the inflation concern does not disappear. The March CPI showed a historically high growth, with price rise covered both food and non-food commodities. A weak USD resulted in significant increase of international commodity prices, further led to a higher production cost. Therefore, CPI is likely to break 6% in mid 2011 driven by the pressure of rise of overall prices. On the other hand, GDP growth declined slightly, but was still within a range of high levels. Net exports and investment have less function in driving the economy. Consumption growth is likely to suffer fall. Thus the economy growth is possibly lower than that of the same period of the previous year. Against this backdrop, a tightening policy is expected to be kept with flexible options in the second half of the year. There is one to two times of interest rate rise in the second quarter together with a lift of reserve requirement ratio. This round of money-driven bounce of bond prices is likely to end. Purchase of medium- and long-term bonds at low prices depends on the impact from interest rate rise. A good opportunity on the bond market requires a signal of shift of the expectation on the microeconomic policy.

Under a cautious market environment, the bank will continue to closely follow the microeconomic situation, mitigate risks in an all-around manner, shorten duration of bonds; seize chances arising from impact of events to earn returns by selling bonds at high and purchasing at low; purchase medium- and long-term bonds at a high yield.

V. Asset Summary of BOC Zhai Shi Tong Wealth Management Plan (March 31, 2011)

| Asset Category |

Net Asset Value (RMB) |

Proportion (to Net Asset) |

| Single fund trust* |

141,762,806.55 |

93.59% |

| Inter-bank lending and bank deposit |

9,706,465.16 |

6.41% |

| Total |

151,469,271.71 |

100% |

Note: Single fund trust refers to "Shanghai Trust - BOC Zhai Shi Tong Single Fund Trust (No.: Shangxin-CB-1107)". The trustee is Shanghai International Trust Co., Ltd., and the custodian for the trust fund is Bank of China Limited.

VI. Asset Summary of Single Fund Trust under BOC Zhai Shi Tong

(March 31, 2011)

| Asset Category |

Proportion (to Net Asset) |

| T-bond |

0% |

| Central bank note |

0% |

| Short-term financing bill |

31.74% |

| Mid-term bill |

63.49% |

| Cash and short-term inter-bank lending |

4.77% |

| Total |

100.00% |

VII. Top 10 Positions under Single Fund Trust of BOC Zhai Shi Tong

(March 31, 2011)

| Bond |

Net Discount/Premium Amortization Value |

Proportion (to Net Asset) |

| 11 Sichuan Expressway CP01(1181104) |

20,000,000.00 |

14.11% |

| 11 Xing Cheng Steel CP01(1181140) |

20,000,000.00 |

14.11% |

| 11 COFCO MTN2(1182071) |

20,000,000.00 |

14.11% |

| 11 Yudean MTN1(1182081) |

20,000,000.00 |

14.11% |

| 11 Yangquan Coal MTN2(1182089) |

20,000,000.00 |

14.11% |

| 10 Jinjiang MTN1 (1082138) |

10,000,000.00 |

7.05% |

| 10 Jiangxi Copper MTN1 (1082152) |

10,000,000.00 |

7.05% |

| 11 CETC MTN1(1182059) |

10,000,000.00 |

7.05% |

| 10 ERDOS CP01 (1081249) |

5,000,000.00 |

3.53% |

Bank of China Limited

April 19, 2011

|