I. Overview

| Product Name |

BOC Zhai Shi Tong Wealth Management Plan |

| Short Name |

BOC Zhai Shi Tong |

| Product Code |

830100 |

| Establishment Date |

May 26, 2010 |

| Product Type |

Non-principal guaranteed, with a variable yield |

| Investment and Returns Currency |

RMB |

| Manager |

Bank of China Limited |

| Custodian |

Bank of China Limited |

| Investment Objective |

This product mainly invests in high credit rating bonds with stable returns and high liquidity on domestic market. With Bank of China as its manager, the investment objective is to provide a bond product with high returns and liquidity and to develop a professional investment channel on domestic bond market by balancing risks and returns and relying on the expertise and investment ability of the bank. |

| Performance Benchmark |

After-tax interest rate of one-year time savings deposit |

| Duration |

None |

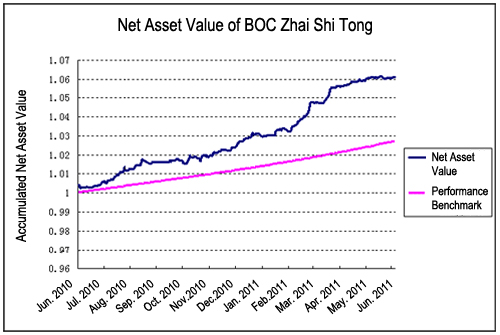

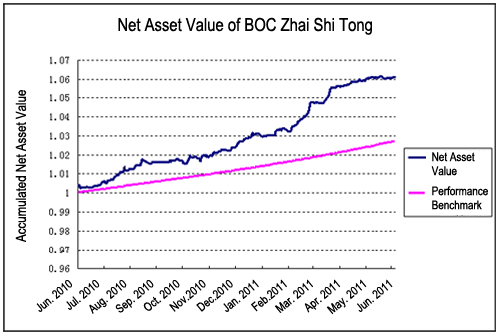

II. Net Asset Value (As of June 30, 2011)

The net asset value and yield of BOC Zhai Shi Tong from its establishment date are shown below (management fee and custodian fee excluded):

| Net asset value per share (June 30, 2011) |

1.0142 |

| Accumulated Dividends |

0.0470 |

| Accumulated Net Asset Value |

1.0612 |

| Annualized yield from the establishment date |

5.58% |

| Performance Benchmark * accumulated yield from the establishment date |

2.68% |

| Accumulated yield - performance benchmark |

2.90% |

Note*: The performance benchmark is the after-tax interest rate of one-year time savings deposit.

The following graph shows the net asset value per share of BOC Zhai Shi Tong against the performance benchmark from the establishment date (May 26, 2010 to June 30, 2011):

III. Bond Market Analysis and Investment Operation During the Reporting Period

The second quarter was characterized by a sharp decline in the market due to the extreme capital shortage and inflationary pressure. The yield on 2-5 year financial bonds increased by 30-40 basis points. However, the yield on 10-year T-bonds did not change much, showing a flatly increasing yield curve.

Faced with the grim situation of inflation, the central bank resorted to a strict monetary policy by raising the reserve requirement ratio for three consecutive months in addition to the April interest rate hike, pushing it to a historical high. The once-in-a-month rise of the reserve requirement ratio this year resulted in over-reserve by the banks, which already had a higher demand for cash at the time of semi-annual performance evaluation. The unexpected raise of reserve requirement ratio on June 20 intensified the bank's shortage in cash and had caused the fluctuation in the monetary market which we witnessed before the Spring Festival with the 7-day repurchase rate topping 9%. Meanwhile, the issuing interest rate of one-year central bank bill was increased 3.5% and had caused the expectation of interest rate hikes. The bond yield curve is on a flat increase. The yield on 2-year central bank bills increased from some 3.6% to around 4%, while the yield on 3-5-year financial bonds increased from some 3.8% to 4.2%-4.3%. However, the yield on 10-year T-bonds only slightly increased from some 3.85% to 4%, then falling back to around 3.9%. The fact that the yield of long-term bonds did not drop significantly indicated that the market was expecting a future economic slowdown and an effective control of long-term inflation by the deflation policies.

It is certain that the fundamental reasons such as an unlikely inflation rate drop caused this round of adjustment of the bond market. The price of pork and vegetables increased significantly in May. The CPI of food showed an apparent year-on-year rise. What drove the rise had shifted from service to non-food consumer products among the non-food CPI drivers, indicating the inflationary pressure from non-food products still existed. The June comparative CPI reached 6.4%. Although the gradual fall-back of the CPI in the second half of the year was an event of high probability, the degree of the fall was uncertain and the peak and duration of the process were likely to be out of expectation. The current macro-economy can be analyzed by the performance of the Troika: a weak export, investment-driven economic structure and a steadily growing domestic demand. Although the actual growth rate of investment has fallen back to the low level since 2003, the investment growth for the second half of the year will be backed by the massive financing need of the entire society and the accelerated investment on supportive housing construction. It is unlikely that the actual growth rate of consumption will continue to drop.

Facing the critical situation of a continuously rising inflation and tighter monetary policies, the manager decisively reduced the holdings of bonds before the sharp fall of the bond market in early June, reducing the proportion of bonds held in the portfolio and the duration to avoid the repercussions resulted from the market decline. We managed to gain on the higher return from the monetary market through short-term lending to ensure a steady increase in the net value of the product.

IV. Outlook of Bond Market and Investment Strategy

The recent interest rate hike at the beginning of the third quarter by the central bank, also the third within the year, did not cause a big change in the yield of the current bonds due to the wide expectation on the market of such moves. In its second quarter regular meeting, the central bank made the announcement for the first time to call attention to the rhythm and intensity of the policies, and had replaced its presentation on the effectiveness of the policies with the stability. The ease on the inflationary pressure is likely to cause the gradual reduction on the intensity of the tightening policy. It is widely believed that the tightening policy is nearing an end and the market will see an apparent reduction in the intensity of the tightening policies in the second half of the year.

We believe that the monetary policy in the second half of the year will depend on the degree of the reduction in the level of inflation. It is the top priority for the government to control the inflation to avoid a negative impact on social stability. Although in the short term, we may not see a dramatic change in the policy, it is likely that we see another interest rate hike in the fourth quarter if the inflation rate exceeds 6% in September and October. The current moderate economic slowdown will not lead to a complete loosening of the monetary policy and a subsequent huge opportunity on the market before the inflation is under effective control. While the bond supply continues to rise in July, the demand by banks and insurance companies is dwindling. In terms of monetary policies, the already high reserve requirement ratio leaves little room for further rise. The government will rely on the open market for taking back liquidity and the difference between the prices of central bank notes on tire I and tire II markets will shrink. From an overall standpoint, the opportunity after a sharp market fall is short-term in nature and should not be viewed as the signal for increasing long-term bond holdings to prolong the duration. Playing defensive shall be our current strategy.

V. Asset Summary of BOC Zhai Shi Tong Wealth Management Plan

(June 30, 2011)

| Asset Category |

Net Asset Value (RMB) |

Percentage (to Net Asset) |

| Single fund trust* |

127,198,917.00 |

95.00% |

| Inter-bank lending and bank deposit |

6,690,965.67 |

5.00% |

| Total |

133,889,882.67 |

100% |

Note* Single fund trust refers to "Shanghai Trust - BOC Zhai Shi Tong Single Fund Trust (No: Shangxin-CB-1107)". The trustee is Shanghai International Trust Co., Ltd., and the custodian for the trust fund is Bank of China Limited.

VI. Asset Summary of Single Fund Trust Under BOC Zhai Shi Tong

(June 30, 2011)

| Asset Category |

Percentage (to Net Asset) |

| T-bond |

0% |

| Central bank note |

0% |

| Short-term financing bill |

4.05% |

| Mid-term bill |

39.08% |

| Cash and short-term inter-bank lending |

56.87% |

| Total |

Total |

VII. Top 10 Positions Under Single Fund Trust of BOC Zhai Shi Tong

(June 30, 2011)

| Bond Code |

Bond Name |

Total Value Assessed by BOC Zhai Shi Tong |

Percentage (of Net Asset) |

| 1081249 |

10 ERDOS CP01 |

5,146,565.00 |

4.05% |

| 1082056 |

10 China Aluminum MTN1 |

29,768,250.00 |

23.40% |

| 1082138 |

10 Jinjiang MTN1 |

9,982,920.00 |

7.85% |

| 1082152 |

10 Jiangxi Copper MTN1 |

9,961,360.00 |

7.83% |

Bank of China Limited

July 13, 2011

|

{kind=link}