I. Overview

| Product Name |

BOC Select Investment Funds Wealth Management Plan 01 |

| Short Name |

BOCFOF1 |

| Product Code |

830082 |

| Establishment Date |

December 17, 2009 |

| Product Type |

Non-principal guaranteed, with a variable yield |

| Manager |

Bank of China Limited |

| Custodian |

Bank of China Limited |

| Investment Manager |

Song Wenbing: Director of the China International Finance Society, postdoctoral researcher of FudanUniversity, holding a Master of Science degree from the Hong Kong University of Science and Technology. Mr. Song has 16 years of working experience in finance, of which 12 years in financial market research, securities investment funds and capital business. He has served as a researcher of the Institute of International Finance, Bank of China; deputy director of the Custodian and Investor Service Department, Bank of China; vice president of BOCI-Prudential Asset Management Ltd. in Hong Kong; senior derivatives trader of the Global Financial Markets Department, Bank of China; and senior investment manager of the Financial Market Unit (agency wealth management division), Bank of China. Mr. Song has been serving as the lead manager of BOCFOF1 investment portfolio since its establishment. |

| Investment Objective |

A steady increase of the asset value of BOCFOF1 over a long term and a yield higher than the performance benchmark by controlling the portfolio risk and maintaining appropriate liquidity with diversified investment in selected securities investment funds. |

| Performance Benchmark |

Yield of SSE Composite Index * 60% + yield of SSE Government Bond Index * 40% |

| Duration |

Non-fixed |

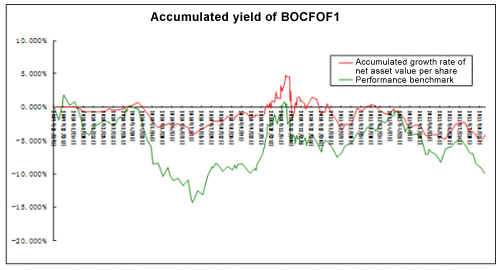

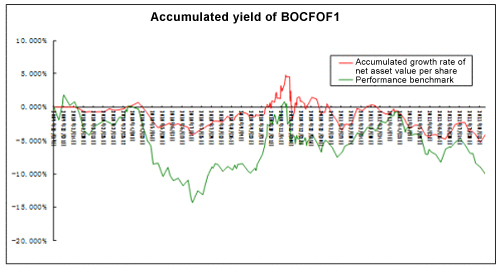

II. Net Asset Value (as of August 19, 2011)

After deducting all fees involved, the net asset value per share of BOCFOF1 is 0.9586 as of August 19, 2011, with an accumulated yield 5.787% higher than the performance benchmark since its establishment.

Source: Wind Info, Bank of China Limited

III. Investment Strategy and Operation Analysis During the Reporting Period

Since 2011, the People's Bank of China has raised the reserve requirement ratio for six times and lifted the interest rate for three times against the growing inflation pressure. However, the tight liquidity at the end of 2010 was relieved along with the relatively centralized disbursement of new loans from banks and the allocation of fiscal deposits in the first quarter of 2011. With eight new measures to curb the property prices launched on January 26, the ever concerned property polices became clear. Driven by cyclical stocks, particularly property stocks, the A-share market bounced back, which then was interrupted in mid April due to the weak momentum under the condition of growing investment, greater inflation and tighter monetary policies. Just the same as the crash in the second quarter of 2010, in particular, the SME Board and ChiNext which rallied significantly in early time suffered the most. Two months later, stimulated by a government official's article published on an overseas media on June 23, the A-share market bounced again. However, the high-speed train crash on July 23 caused a slump of concept stocks related to high-speed train, as well as a sharp fall of cyclical stocks related to investment. The broad market dropped after the consolidation. With the U.S. sovereign credit rating downgraded by Standard & Poor's on August 8 and the European sovereign debt crisis deteriorated, the global stock markets tumbled sharply following the U.S. and European markets, and the A-share market also dropped abruptly, and then bounced back a little thanks to the intervention from the hunters' capital. Most institutions thought there was no room for higher inflation and interest rate, but the concern about the interest rate rise appeared again as the July CPI created a new record high, and the interest rate to issue 3-month, 1-year and 3-year central bank notes rose. Furthermore, the U.S. and European stock markets tumbled again due to the worse-than-expected U.S. employment data and tighter liquidity in the eurozone financial system. Consequently, the A-share market dropped with gap opened, being challenged by the possibility of early low again.

Against the backdrop of management of inflation expectation, it is thought the overall tighter liquidity is the key constraint to the A-share market. On the other hand, the staged margin improvement of market capital will bring out opportunities in certain sectors. Based on the analysis on the macroeconomic situation in early 2011, the non-ferrous metal stocks and coal and building materials stocks are overweighted appropriately, and some funds are replaced in late January, thus the product is benefited from the market bounce in the first quarter. Being underweighted in early April, the product is less influenced by the market slump. After skipping the short-term bounce starting on June 23, the product is overweighted in the panic of market slump on August 8 and 9. According to the product manager, after this panic, the risks in the A-share market are mitigated obviously, thus it is a right time to strategically overweight and adjust the portfolio. The product is mainly invested in the individual stocks and active funds targeting the growth stocks with comparative advantages. According to the data from Wind Info, the product has a performance better than other products of its kind established in the market on the same date.

IV. Market Outlook and Investment Strategy

Following a slump in the A-share market, now it is worth investing in the market in a historical view. Although it takes time for the investors to resume the confidence in the market, and it is likely to test the historical low in the near future (even a new record low may be created), it is thought the broad market has been approaching the safe bottom zone. In the coming months, the inflation pressure will be relieved on the basis of the analysis of the inventory de-stocking process, this round of inflation caused by commodity and food prices and other key factors. There is a high probability of deflation after August, and a low probability to continue the quantitative tightening monetary policy by the central bank after considering the credit bond fund event in July and the complicated international situation. However, it is unrealistic for the central bank to ease the monetary policy in the coming months, and there is a time lag from the highest inflation pressure to the action of the stock market. Furthermore, a global deleveraging is carrying out at the government level, the growth rate of global and Chinese industrial production is falling, and the commodity prices are falling after touching the high. There is no catalyst for the rise of the highest weighted cyclical stocks, and it is possible that some consumer stocks may fall after a great rise in early time. All these factors show that the overall market will be in the process of capital stock movement in the coming months, and it is difficult for the broad market to perform well. It will be a course of bottom, which might be tough and long under the background of inflation expectation management and economic structure transformation. Nevertheless, the growth stocks with the comparative advantages and the active funds targeting such stocks with more flexibility of selection will hopefully become the focus in the market in the foreseeable future, enabling the investors to see the light at the end of the tunnel.

V. Asset Summary (August 19, 2011)

| Asset Category |

Proportion |

| Deposits |

6.69% |

| Monetary market fund |

9.80% |

| Subtotal of monetary assets |

16.49% |

| Bond fund |

17.18% |

| Subtotal of bond assets |

17.18% |

| Stock-type open-end fund |

31.28% |

| Close-end fund |

14.95% |

| Index fund |

1.53% |

| Stocks |

18.58% |

| Subtotal of equity assets |

66.33% |

| Total |

100.00% |

VI. Top 10 Holdings (August 19, 2011)

| Asset Name |

Proportion |

| China Southern Select Growth Fund |

8.79% |

| UBS SDIC Moderate Growth Fund |

8.69% |

| BOC Moderate Enhanced Bond Fund |

8.60% |

| Changsheng Tongsheng Fund |

6.19% |

| Harvest Value Advanced Equity Fund |

5.91% |

| ICBCCS Enhanced Income Bond Fund A |

4.45% |

| Huashang Strategic Select Fund |

4.14% |

| CCB Principal Stable Income Bond Fund |

4.13% |

| HFT Leading Growth Equity Fund |

3.74% |

| CCB |

3.67% |

| Total |

58.32% |

Bank of China Limited

August 19, 2011

|

{kind=link}